The euro-dollar pair has been trading in the price range of 1.1580-1.1650 for the second week in anticipation of key fundamental events. Let me remind you that tomorrow we will know the results of the October meeting of the European Central Bank, and next week - the results of the November meeting of the Federal Reserve. On the eve of these events, traders do not dare to open large positions, taking profits when approaching one of the boundaries of the above range. As a result, the pair walks in a circle, reacting reflexively to the current news stream.

It is worth noting that on Thursday, the attention of market participants will be focused not only on the ECB, but also on US macroeconomic reports. In particular, key data on US economic growth in the third quarter will be published tomorrow. Given such a busy calendar, traders need to fasten their belts in anticipation of increased volatility.

Unlike previous ECB meetings, on the eve of which analysts only speculated how dovish the mood of the members of the Governing Council would be, the October meeting holds a certain intrigue. And although, in my opinion, the hawkish hopes of traders look absolutely far-fetched and groundless, such aspirations of some market participants cannot be ignored.

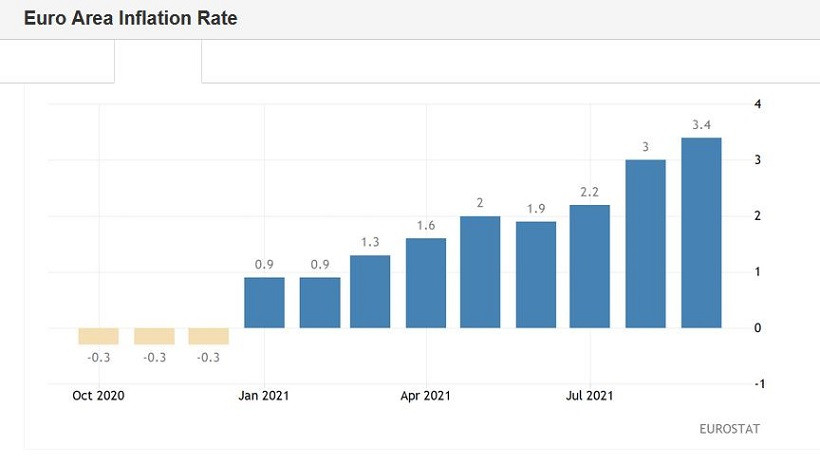

Cautious talk that the ECB may shift the expected timing of an increase in the deposit rate to the beginning of 2023 (some even admit the option of the second half of next year) appeared three weeks ago, after the release of data on inflation growth in the eurozone. Moreover, such discussions among the expert community did not stop even after the dovish comments of a number of ECB representatives. European inflation really jumped up in September (once again), reaching multi-year highs. The overall consumer price index was 3.4% in September (after rising to 3.0% in August), and the core index, excluding energy and food prices, jumped to 1.9%.

Inflation indicators have been growing for several months in a row, fueling rumors that, firstly, the ECB will begin to reduce the volume of asset purchases from November, and secondly, it will allow the probability of a rate hike earlier than 2024. Supporters of the hawkish scenario also point to the fact that the ECB, following the results of the September meeting, raised its forecast for eurozone GDP growth. According to central bank economists, the economy will grow by 5%, which is higher than the June forecasts (4.6%). The forecast for inflation growth in the region has also been raised: for the current year - to 2.2% (from 1.9%), for 2022 - to 1.7% (from 1.5%).

Hawkish expectations keep the single currency afloat, allowing EUR/USD bulls to organize counterattacks to the upper limit of the 1.1580-1.1650 range. Of course, if ECB President Christine Lagarde really sounds hawkish notes tomorrow, the single currency will shoot up throughout the market, and the EUR/USD pair will not be an exception here. But in my opinion, euro supporters will be disappointed tomorrow, which is fraught with a deep downward pullback.

To begin with, one of the most influential members of the ECB, Philip Lane (chief economist of the central bank), recently commented on the hawkish mood in the market. He stated that traders are wishful thinking, complaining at the same time about the weak level of communication. He made it clear that market expectations do not correlate with the intentions of the central bank. I believe that this message will be repeatedly voiced tomorrow, in one form or another.

Another representative of the ECB - the head of the Bank of France Francois Villeroy - continues to insist that the current increase in inflation in the eurozone is temporary, and, therefore, the ECB needs to be patient not to take hasty steps.

Here it is necessary to recall Lagarde's October statements. Commenting on the latest macroeconomic releases, she reiterated her thesis that the ECB's new strategy allows for a temporary excess of the inflation target, allowing the central bank to ignore a temporary inflationary surge. By and large, the ECB offset the value of inflation growth in the eurozone in advance, convincing the markets that the central bank would not react to these trends. At the same time, Lagarde again voiced the mantra that the current price increase is temporary, and medium-term inflation is "significantly below the target." The head of the ECB noted the improvement in the labor market (the unemployment rate is indeed consistently decreasing), but at the same time drew attention to weak wage growth and the cautious position of consumers. According to her, "these factors are of concern to the ECB."

Well, in addition to the words of Lane/Villerois /Lagarde, you can recall the latest reports from the PMI and IFO. In particular, the indicator of the conditions of the business environment in Germany in October was in the red zone, dropping to 97.7 points (against the forecast of a decline to 98.2 points). This figure has been consistently declining for the fourth consecutive month, reflecting the pessimism of German entrepreneurs. The indicator of economic expectations from IFO also showed negative dynamics. The indicator came out at around 95.4 points - this is the weakest result since February this year. The preliminary PMI indices for October were also published last Friday, which also turned out to be rather weak. For example, the German PMI in the services sector came out at around 52.4 points - the weakest result since April.

Summarizing all of the above, we can ask one single question: is there at least one weighty argument that will force the representatives of the dove wing of the ECB to change their position? In my opinion, tomorrow the ECB will quite categorically refute all hawkish assumptions, announcing in passing that the curtailment of the PEPP program in July next year "will not be the end of the accommodation policy."

It is most advisable to take a wait-and-see attitude on the EUR/USD pair until the end of tomorrow, given the fact that, in addition to the announcement of the results of the October meeting of the ECB, key data on the growth of the American economy for the third quarter will also be published tomorrow. These events can provoke, so to speak, "emotional volatility", increasing the risk of false price movements. In the medium term, in my opinion, the priority will remain with the downward scenario, but if we talk about tomorrow, then impulse price shots are possible here, which can lead to losses.

The material has been provided by InstaForex Company - www.instaforex.com