EUR / USD

The euro continues to fall unexpectedly. Over the past 6 weeks, the decline further lower than 750 points and reaches the levels of July last year this time. The rate of decline corresponds to previous review in August 2014, when the eurozone crisis was spiraling upward on the spearhead with Greece and Cyprus. Now, we see a situation almost similar since the US is in conflict with Europe, Russia, Syria, Iran, North Korea, China and even Mexico and Canada at the same time. And, it is the regulated growth of the dollar on the basis of geopolitical tensions which is the main reason for the ongoing processes in Forex. Above all, like the growth of bond yields, macroeconomic indicators, dollar restriction and other reasons are secondary important although important and interrelated, and, if necessary, breaking traditional correlations. The political and economic struggle in the US happened against the backdrop of a strong dollar, as Trump spoke about in his election campaign and which became the talk for about the past six months. A number of inconsistencies and internal obstacles in the US itself, including the struggle with Trump of forces opposing it, have postponed this large-scale plan for several months. In the medium and long term, we are expecting the euro at 1.01 up to 0.8350, as mentioned in the May 14 article"Long-term perspective of the euro".

Yesterday, investors' moods to sell the euro increased with the release of unfavorable economic data for the single currency. The business activity index in the service sector (Services PMI) of the euro area for May showed a decrease from 54.7 (revised down from 55.0) to 53.9. While Manufacturing PMI declined from 56.2 to 55.5 versus expectations of 56.1. On the contrary, the US Services PMI increased from 54.6 (revised upward from 54.4) to 55.7, and Manufacturing PMI increased from 56.5 to 56.6 (at the forecast level). The consumer confidence index of the euro area in May remained at zero level. US sales of new homes in April amounted to 662 thousand against expectations of 680 thousand, but the mood of investors for sales was already strong.

The Fed's FOMC minutes of meeting to be released late in the evening confirmed that the rate will be raised in June ("... continue ... raising rates"), however, the markets along without additional statement presented a 100% rate hike at the nearest meeting, the quotes failed to achieve.

Today, Germany's GDP will be released for the first quarter in the 2nd assessment, with the forecast remained unchanged at 0.3%. The consumer climate index in Germany GfK for June is also expected to be unchanged at 10.8 points. At 12:30 PM London time, FOMC minutes will be issued from the last ECB meeting. But, investors with even greater confidence do not expect to see new information.

In the United States, the number of applications for unemployment benefits for last week is expected at 220,000 compared with 222,000 earlier. The house price index for March is expected to be 0.5% after 0.6% in February. Sales of homes in the secondary real estate market in April are forecasted by 5.56 million versus 5.60 million in March. The mood for euro sales is secured.

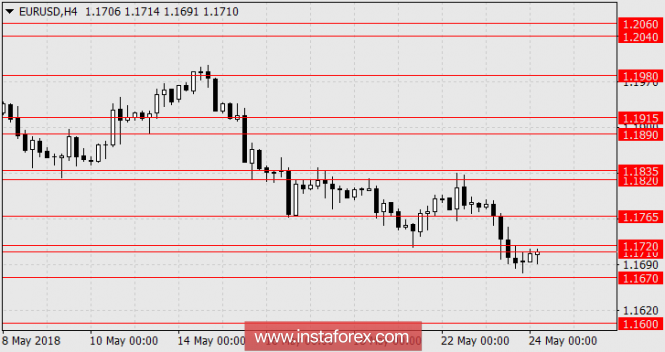

We are expecting for the single currency at 1.1600.

* The presented market analysis is informative and does not constitute a guide to the transaction.

The material has been provided by InstaForex Company - www.instaforex.com