EUR / USD

Yesterday's events in the market went according to the expected and obvious scenario. Weak German GDP against the backdrop of crisis-low ZEW indexes and good retail sales figures in the US sent the euro to its peak.

Expectations on Germany's GDP for the first quarter were 0.4% versus 0.6% in the fourth quarter, but the economy showed an increase of only 0.3%. The German business sentiment index ZEW for May remained at the previous April level of -8.2 against the expectation of a slight increase to -8.0. Industrial production of the eurozone as a whole in the March estimate added 0.5% against expectations of 0.6%, and the previous figure in February was revised down to -0.9% from -0.8%. Against this background, the second estimate of the euro area's GDP of 0.4%, which came at the expectation level (against 0.6% in the fourth quarter), was already perceived as good news. As well as the growth of the index of sentiment in the business circles of the eurozone ZEW for May from 1.9 to 2.4.

Retail sales in the US for the month of April increased by 0.3% against expectations of 0.4%, but the March growth was revised to increase from 0.6% to 0.8%. Basic Retail Sales added 0.3% against the forecast of 0.5% but here, the previous indicator was increased from 0.2% to 0.4%. At the same time, the sales in large stores increased from 4.2% y / y to 4.9% y / y, which demonstrates the obvious desire of consumers to spend more without significant savings in online stores. The index of business activity in the manufacturing sector of New York for the current month rose to 20.1 from 15.8 in April. The forecast assumed a decrease to 15.1. Business activity in the housing market from the NAHB in May rose to the expected 70 points.

The dollar-linked commodity assets also fell significantly: gold -2.23%, copper -1.26%, silver -2.28%, oil -0.07%, and wheat -0.50%. The breakthrough of the dollar, therefore, took place. And the shift in investor sentiment can be called "tectonic", as the yield on 10-year US government bonds reached 3.09%, and the market expectation of the rate for December of this year was 2.23%, which means almost 100% confidence in a 3-fold rate increase and a 52% expectation of a 4-fold increase. In this light, it is logical that the stock market decline (S & P500 -0.68%) is a closing of long positions at the burst of expectations of the strengthening of the rate of monetary policy tightening.

In Italy, President S. Mattarella postponed the issue of forming a government for the next week, increasing the parliamentary factions time to think over the situation.

Today, the final estimates of the euro area CPI for April are the same with the forecast without changes: 0.7% y / y for core inflation and 1.2% y / y for the total. For the United States, we again expect positive indicators. The volume of industrial production for April is projected to grow by 0.5%. The capacity utilization factor is expected to increase from 78.0% to 78.4%. The number of housing permits for new homes in April is expected to be 1.33 million y / y against 1.32 million y / y a month earlier. The number of issued permits for the construction of a new house is expected at the previous level of 1.35 million.

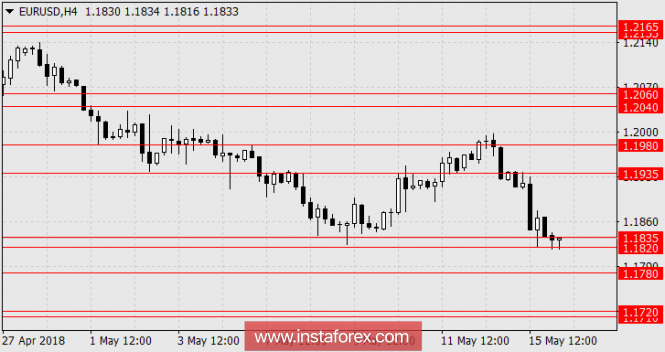

We are waiting for the euro in the range 1.1710 / 20.