The dollar showed mixed dynamics during trading on Friday and did not have a definite direction. After the FOMC raised its market expectations for a December rate hike up to 70% by its rather aggressive statement on Wednesday, investors on Friday weighed in the speeches of three Committee members who disclosed details of their outlook for the situation.

The head of the Federal Reserve Bank of San Francisco, John Williams, said that he does not expect serious shocks in the markets because of the beginning of the policy of normalizing the balance sheet. The Fed has already announced its intentions for quite some time, the markets have taken into account the plan, and now it only needs to carefully monitor the development of the situation. On the topic of rates, Williams expressed complete agreement with the forecast of the Fed, saying that he sees a long-term goal of the interest rate at 2.5% for two years and suggests that the rate will be raised again this year and three times in the next.

A little later, the head of the Federal Reserve Bank of Kansas, Esther George, almost verbatim repeated the main arguments of Williams, adding that postponing the tightening of the policy could create risks in the long term, and called for dismissal of the low inflation rates, as "wages grow faster than prices." Meanwhile, President of the Federal Reserve Bank of Dallas Robert Kaplan added that aside from strengthening the "cyclical inflationary pressures," it is necessary to take into account the structural changes in the economy associated with the transition to a new technological level that offsets inflationary pressures.

Thus, the leadership of the Fed demonstrates a united stance, and there is no internal discussion that could call into question the implementation of the plan. Also, there is no concern that there will be four vacancies in the Fed soon. Vice-Chairman Stanley Fischer will resign in October, and Janet Yellen's term will expire in February. Obviously, the markets are not afraid of interference in the policy of the Fed, particularly by Donald Trump, who during the pre-election race, subjected the Fed's policy to rather serious criticism.

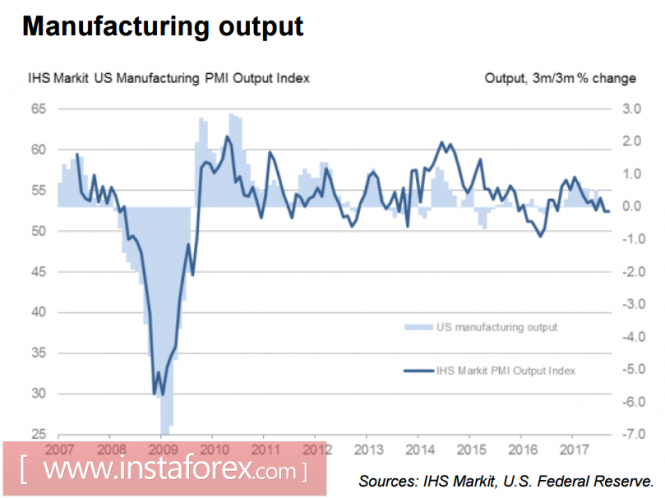

Meanwhile, the preliminary reading of PMI Markit in the services sector was just below expectations and came in at 55.1p in August, against 56.0p a month earlier. The moderated expansion continues in the manufacturing sector, the index increased from 52.8p to 53.0p, but in the indicators of orders there is a clear stagnation - there is no growth export sales, new orders have minimal growth rates for the year, as well as output.

Markit analysts attribute some slowdown to the impact of the hurricane, which led to a temporary disruption in production and a rise in raw material prices due to supply issues, and believe that a temporary slowdown should not be given much bearing. GDP growth rates in Q3 are also unlikely to be high. In any case, the GDPNow model from the Atlanta Federal Reserve Bank forecasts a 2.2% growth, which looks clearly unconvincing, especially after the Fed raised its GDP forecast for the current year.

This week, special attention will be directed to the publication of the PCE deflator for August and data on personal incomes and expenditures on Friday. The report can have a significant impact on the expectations of the dollar, as it will allow the assessment of the level of inflation. Also, in the current situation, a positive dynamics is necessary for personal incomes,as its absence will cast doubt on the position of the Fed, which expects inflationary pressures to be strengthened by outpacing growth in wages.

On Wednesday, a report on orders for durable goods in August will be released. Despite the fact that consumer confidence has been declining in recent months, it remains at confidently high levels, and the trend towards the growth of large purchases by consumers can indicate changes in consumer sentiment.

The dollar completes the months-long period of weakening. The market will not ignore the Fed's position and will wait for support from macroeconomic indicators, as well as news about tax and medical reform. These developments have highest chances to show growth in the dollar against the yen, the franc and the euro.

The material has been provided by InstaForex Company - www.instaforex.com