Encouraged by hopes of stimulating the US economy under the influence of Donald Trump's stimulating programs, the "bears" of the EUR/USD pair went into a counter-attack. The consequences of hurricanes "Harvey" and "Irma" were not as terrible as initially expected. Besides, history shows that "Katrina" was stronger against the two, at a time when the Fed raised the federal funds rate in 2005. Natural disasters are temporary and in the end the result of the restoration work can benefit the GDP. Simultaneously, the idea of tax reform, which in late 2016 pushed up the USD index, has returned to the market.

Judging by the comments of the Republicans, the bill on changes in the taxation system will become public for a week by September 25. Up to this point, one can only guess at the basic provisions of the reform and how far it will spread in the American economy. The president only hinted that the rich should not expect special preferences, which contrasts with previous statements about the reduction of corporate tax and real estate tax. However, the fact that Trump changes his mind like a glove, throughout it should be expected.

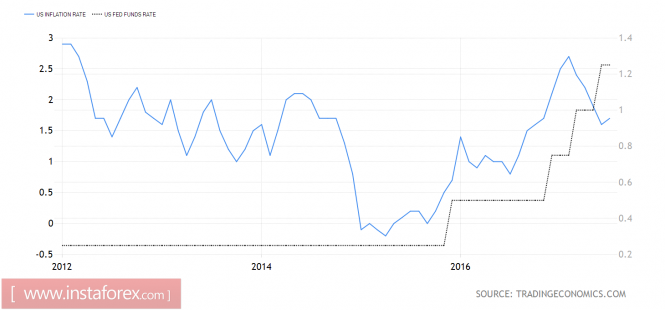

The rise in US GDP growth rate entails a more rapid tightening of the monetary policy by the Fed, compared with what the markets are currently waiting for. While the regulator is concerned about inflation, it must be understood that conditions are constantly changing. If in the 1970s, its average level was 7.1%, in the 1980s - 5.6%, in 1990 - 3%, in the 2000s - 2.6%, but now it is below the 2% mark. The liability is globalization and new technologies that increase competition and force producers to cut prices. In correlation with this, raising the federal funds rate to 3-3.5% or higher, as it was before, is not necessary. The cycle of monetary restriction of the Fed can be completed much earlier, and the realization of this fact will attract new sellers of the US dollar to the market.

Dynamics of inflation and federal funds rates

Source: Trading Economics.

The outlook for the euro, on the contrary, appears optimistic. In fact, due to the lag in the economic cycle in the eurozone compared to the United States, the ECB is at the same pace as the Fed in 2014. The European Central Bank is ready to normalize monetary policy, and the current EUR/USD pair correction only increases the likelihood of it. In October, Mario Draghi will report on the curtailment of the quantitative easing program. This will be a new occasion to buy the euro.

It should be noted that during its last cycle of tightening monetary policy in 2005-2008, the regional currency strengthened against the US dollar by 30%, and if history repeats itself, the current +13% is just the beginning. In this regard, it makes sense for traders to stick to the previous strategy in the main currency pair - buying on payoffs.

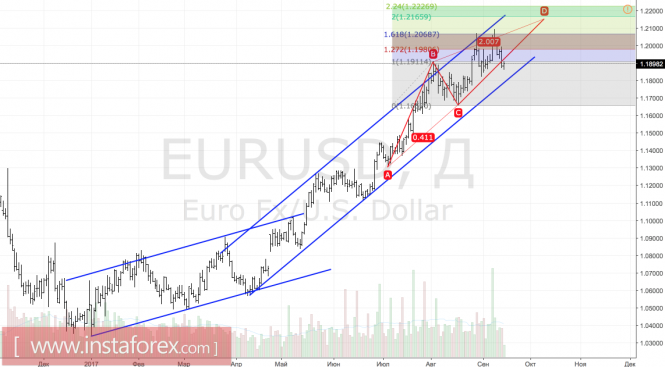

Technically, the inability of bulls to move prices above the target by 161.8% on the AB = CD pattern indicates their weakness. The formation of the double vertex increases the correction risks in the direction of at least the lower boundary of the upstream trading channel.

EUR/USD, daily chart