The US dollar finished the week with a decline and without compelling reasons to resume growth.

Published on Wednesday, the FOMC protocols should not have had a significant impact on the quotes but the markets nevertheless drew attention to the fact that the topic of low inflation in the discussion of current policies caused increased concern on the Cabinet leadership. The same conclusion was confirmed by Janet Yellen in one of her last speeches as the head of the Fed. She said that there are doubts among FOMC members that low inflation is temporary.

Weak consumer activity was confirmed in the report on orders for durable goods for the month of October. Instead of the projected growth of 0.3%, there was a fall of 1.2%. By Friday, the markets was in a state of confusion. It could be expected that the closing of the week will contribute to the demand for the dollar but the IFO report on Germany led to a sharp increase in the euro with business sentiment growing more than expected. The report published yesterday showed that GDP growth in the euro area could rise to 2.3% which may eventually stimulate the ECB to take more active measures to normalize monetary policy.

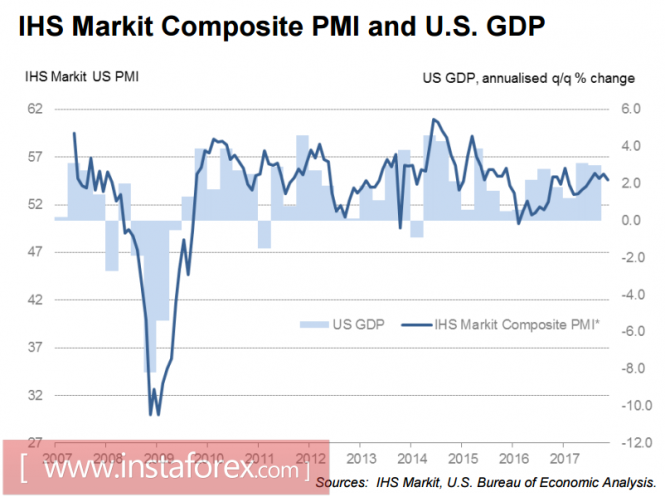

Activity in the US is slowing down. The PMI composite index for Markit declined in November to 54.6p. This is a 4-month low. The growth in activity in the services sector and in the manufacturing sector has also slowed.

Trumpomania, which recently created a positive mood in the US economy, is clearly starting to slip. The time of expectations is over and the harsh routine begins. The Fed's policy aimed at gradual normalization should be based on a growing economy but the market does not yet see stable growth signals, except perhaps in the labor market. However, the record low unemployment does not contribute to the growth of purchasing activity. Wage growth is not enough to create the prerequisites for inflation which in the end, may cast doubt on the ability of the Fed to withstand the schedule.

On Wednesday, the second preliminary estimate for US GDP growth in the third quarter will be published. Experts are optimistic and predict a revision from 3.0% to 3.2%. The dollar, in turn, can receive the long-awaited support. Also, the price index for Q3 is expected to be revised from 2.1% to 2.2%. Meanwhile, the index of personal consumption expenditure is of special interest and a revision of it in any direction can push the dollar into motion.

On Thursday, data on real spending on personal consumption for the month of October will be published and positive dynamics is absolutely necessary here. The forecasts are rather pessimistic. It is expected that expenses will grow by 0.3% with a relative to growth by 1% in September. The revenues are expected to grow by 0.3% against 0.4% a month earlier. The slowdown will have a negative effect since it will further reduce inflation expectations and put the Fed in a difficult position, as justifying the rate hike in December will not be easy.

The key day is Friday. Markets traditionally focus on business activity indices from ISM and record growth in recent months contributed to the growth in demand for the dollar. In addition, stock markets have updated to historical highs but Markit shows a completely different picture and therefore the slowdown of indices from ISM is becoming more and more likely.

Thanksgiving Day prevented the release of the weekly CFTC report. The release was postponed to Monday and this time, the attention to it will be high. The last 6 weeks dynamics in the mood of long-term investors was in favor of the dollar, which allowed us to count on its growth. However, the prolonged period of weak inflation can contribute to a change in sentiment. If on Monday, the report shows a slowdown in demand for the dollar, especially against the defensive currencies, this will signal further growth for the yen and the euro against the dollar and significantly complicate the bullish mood.

The material has been provided by InstaForex Company - www.instaforex.com