The Federal Reserve continues to pump markets with liquidity. The Fed's balance sheet grew by $1.7 trillion in less than a month, and the monetary base by more than $1 trillion. Despite the fact that all this cash is in demand at the stage of deepening the crisis, such steps for the dollar can not pass without a trace.

Expansion of the Fed's balance sheet after the 2008 crisis led to a significant saturation of the market with dollar liquidity, but then an excess of liquidity weakened the dollar, and US economic growth slowed its recovery. In the last month, the Fed uses the same methods, but much more aggressively, the balance before the end of this year may well reach the level of 9-10 trillion.

We should also assume that the global yield has collapsed this year, and the US has lost any advantage in terms of yield over other currency zones. It is no accident that CFTC reports show that in recent weeks speculators are moving away from the dollar, because they expect that after the first signs of stabilization appear, excessive dollar liquidity will inevitably lead to its fall.

Only the global OPEC++ deal involving the United States, Canada, Mexico and the United Kingdom can make significant adjustments to the current situation, but the chances of such an outcome are very small. The decline in production will occur, but only after there is strong evidence of a global decline in industrial production.

EURUSD

Europe is facing a real threat of division. On the eve of the meeting of EU finance ministers, Italy approved the so-called "liquidity decree" worth 400 billion euros, bringing the amount of financial obligations of the government to 750 billion euros, and all this – without the approval of the EU. At the same time, a group of EU countries led by Germany insists on a single aid mechanism that should be linked to future economic reforms, and until this happens, no crown bonds can be issued.

Therefore, the eurozone is not yet able to release liquidity to the markets that would cover the supply of the dollar. A significant gap in the supply will push up the European currency, growth to the resistance zone of 1.1050/70 is justified, then the goal of 1.1150, in the medium term, the euro will strive to the upper limit of the channel 1.1310/40.

GBPUSD

Industrial production in Great Britain restrained itself from a deep fall in February, and the decline was only 2.8% y/y, which turned out to be even slightly better than expected. At the same time, the trade balance with countries outside the EU fell to -5.573 billion pounds, with a forecast of -0.5 billion, and this, apparently, is only the first sign of an impending economic catastrophe.

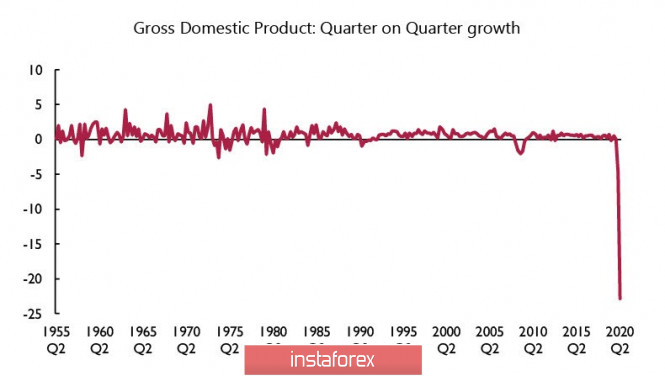

NIESR estimated the fall in GDP for three months through February inclusive at 0.1%, but voiced much darker forecasts for Q2. In their opinion, quarantine causes the largest reduction in economic activity since 1921, and GDP is projected to decrease by 5% in the first quarter and by 15-25% in the second. The chart from the NIESR report speaks for itself:

Under current conditions, no financial institution undertakes to give a reasonable forecast of both the depth of the fall and its length over time. NIESR suggests that the main blow will be in sectors such as trade (40%), transport (40%), production (30%), construction (30%), while the financial sector will suffer by 10%, and mining minerals - by 5%. The last point is somewhat surprising - against the backdrop of a global decline in oil demand, OPEC+ countries are already negotiating a reduction in production from 10% to 30%, and the UK is going to lose only 5% in the sector as a whole.

Be that as it may, we must proceed from the fact that the pound has no internal resources for growth. GBPUSD has again approached the resistance zone 1.2560/80, which it has been unsuccessfully attacking for two weeks, and technically the possibility of going higher to 1.2870/2910 looks rather likely. But from the point of view of the overall fundamental picture, there is no reason to believe that the pound will be able to win amid a global fall in demand for resources. The likelihood of a decline to 1.2150/2200, that is, a departure to the side range, is much more justified.

The material has been provided by InstaForex Company - www.instaforex.com